It’s a perfect place to discover tips on how to launch your online business and sell online virtually everything. From time to time, you’ll get updates on the shopping cart we develop with so much love.

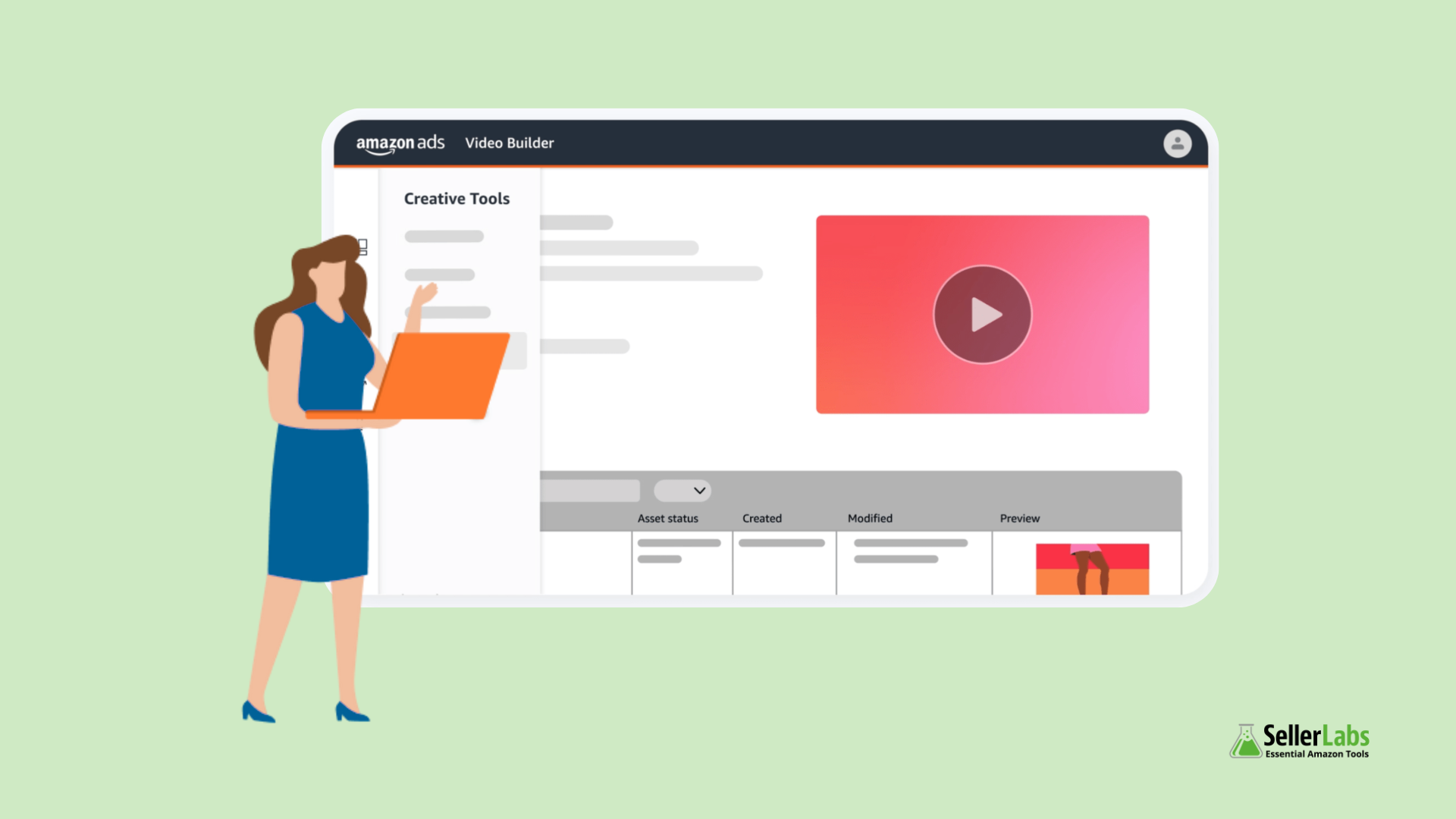

“It’s not just about listing your product anymore—it’s about bringing it to life.” In 2025, selling on Amazon means competing in a marketplace driven by scrolls, swipes, and split-second decisions. A killer headline? Helpful. A clean image stack? Necessary. But the secret weapon? Video. Now, with Amazon Video Builder (Beta), you can create engaging, professional […]

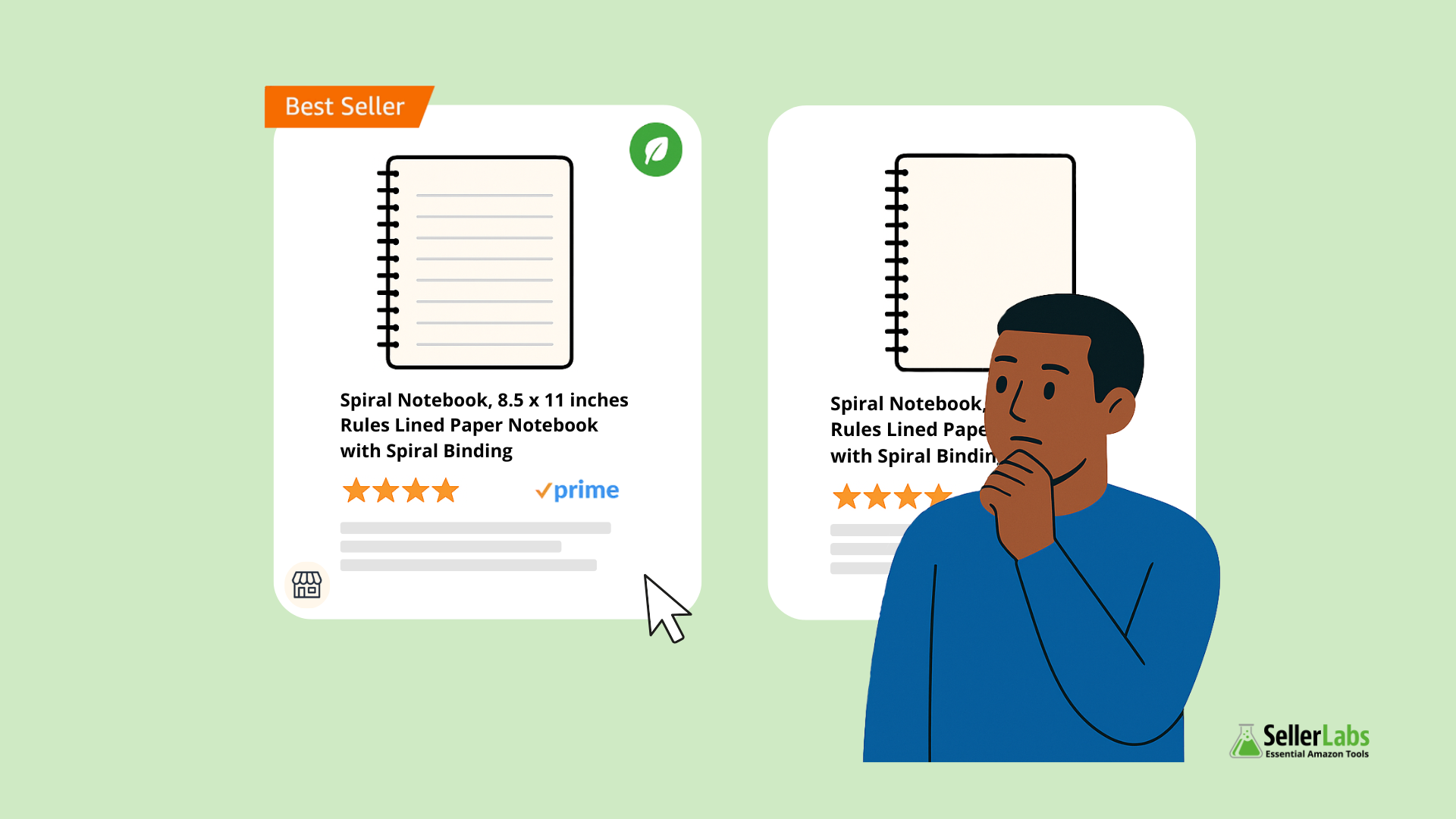

What if one small badge could double your conversions? In 2025, Amazon badges aren’t just decoration — they’re decisive. From the Best Seller and Amazon’s Choice badges to new program-driven badges like Climate Pledge Friendly and Small Business, Amazon’s visual trust signals are doing a lot of heavy lifting. These badges are more than flair […]

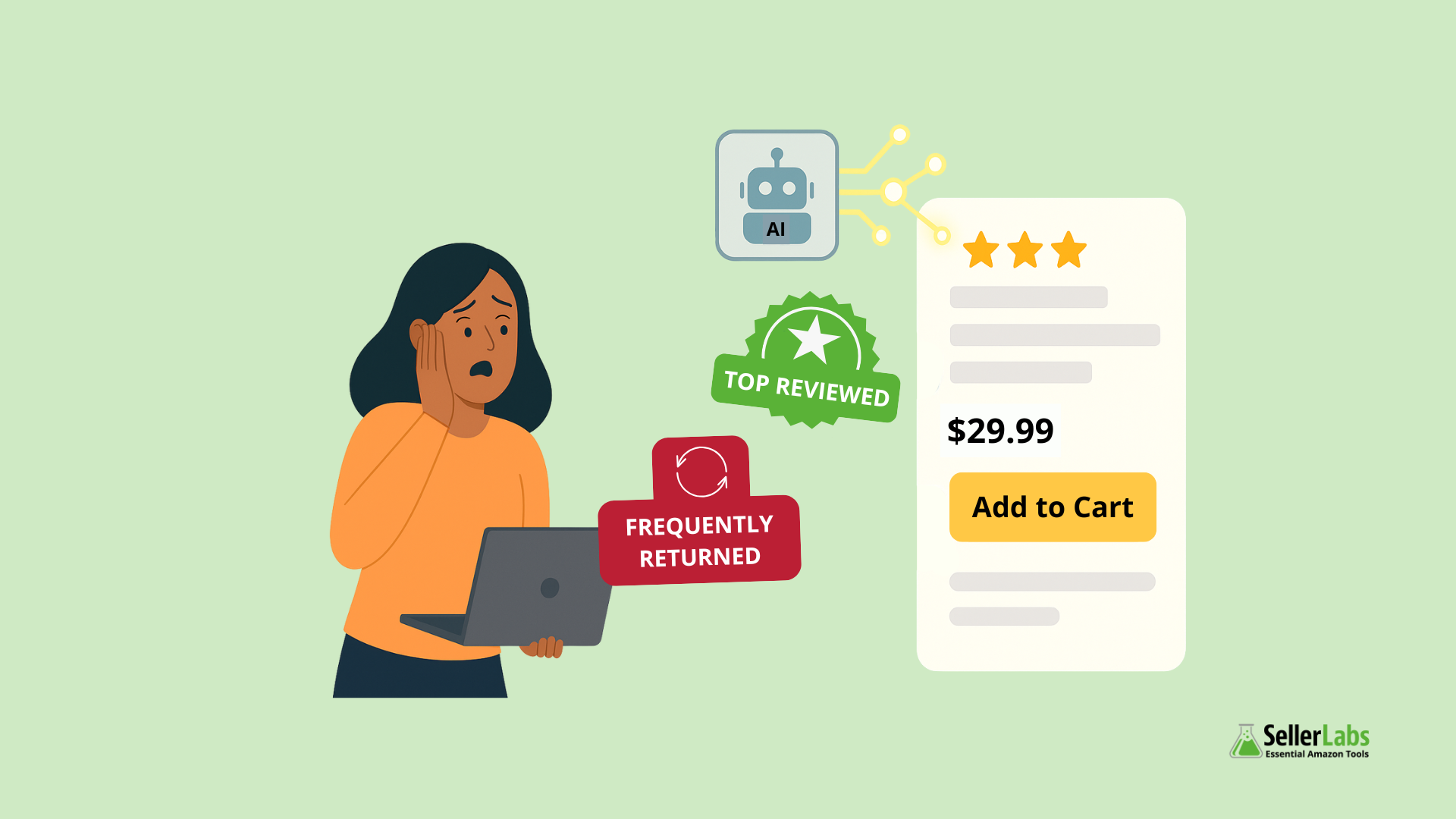

“You won’t beat AI by ignoring it. You’ll beat your competitors by using it better, faster, and smarter than they do.”— An Amazon Seller after losing a badge overnight Chapter One: The Wake-Up Call Imagine this: You’ve just spent two weeks writing the perfect listing. Bullet points are polished. SEO is dialed in. Images are […]

Why Amazon Sellers Should Pay Attention In 2025, Walmart Marketplace isn’t just playing catch-up—it’s accelerating fast. From major platform updates to rising third-party seller adoption, Walmart has emerged as a serious channel worth watching. If you’re an Amazon seller feeling squeezed by rising fees, storage restrictions, and unpredictable catalog issues, it might be time to […]

When Amazon Silence Hurts Your Sales Imagine this: One of your best-performing listings suddenly disappears without warning. You reach out to Amazon Seller Support, explain everything clearly, and wait. Days pass. No resolution. Your sales plummet. You’re stuck. This is a reality for thousands of Amazon sellers every year. Whether it’s an unexpected account suspension, […]

📅 Confirmed Prime Day Dates: July 8–11, 2025 Amazon has officially announced that Prime Day 2025 will run from July 8 through July 11. That’s four full days of high-converting traffic, increased buyer intent, and a surge in demand across every category. With the event arriving earlier than many sellers anticipated, the next three weeks […]

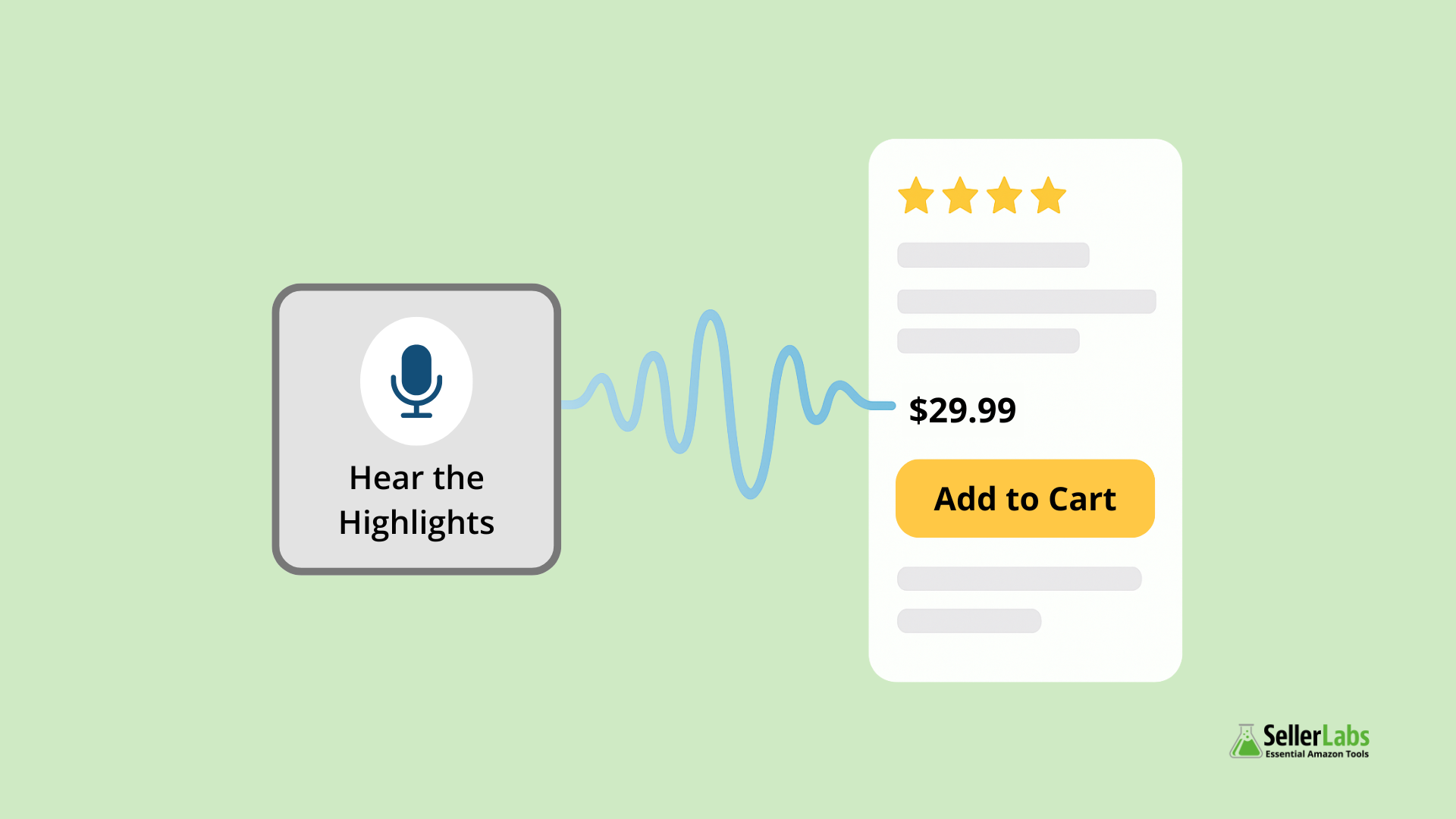

Amazon’s latest test feature—“Hear the Highlights”—isn’t just another flashy update for shoppers. It’s a clear signal that voice-first ecommerce is on the rise, and sellers who prepare now will have a powerful edge. Powered by generative AI, this new audio feature is already being tested on select products in the Amazon Shopping app, offering short-form […]

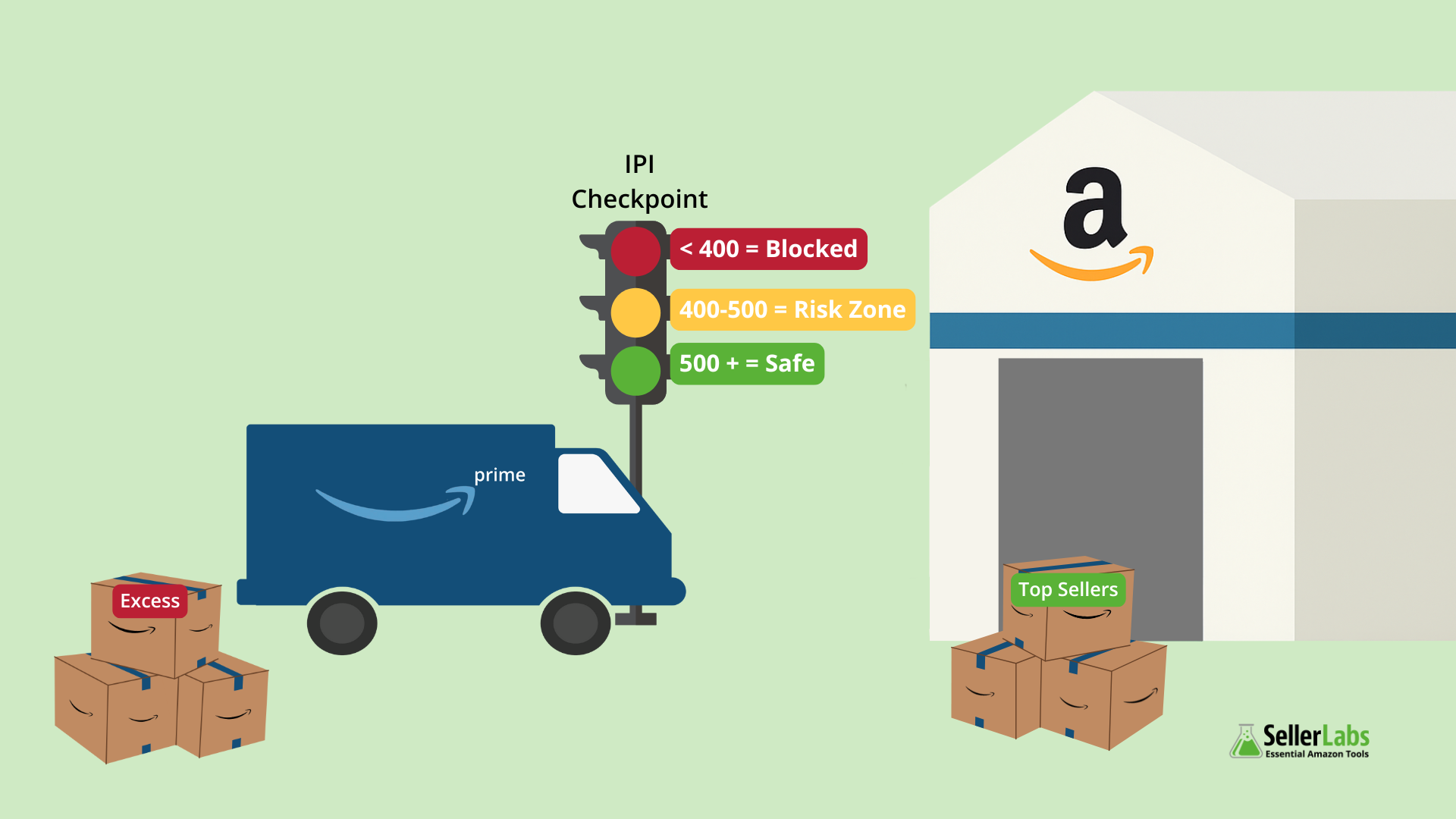

If you’re an FBA seller, your Inventory Performance Index (IPI) score is more important than ever in 2025. With Amazon tightening inventory restrictions and raising fees, ignoring your IPI score can lead to costly consequences like storage limits, higher fees, and blocked shipments—every seller’s nightmare. So how does the IPI score work in 2025? What’s […]

Thinking about starting your Amazon business in 2025? You’re not alone—and you’re right on time. With over 300 million active Amazon users and third-party sellers now driving over 60% of all product sales, selling on Amazon has never been more promising. But success isn’t as simple as listing an item and hoping for the best. […]

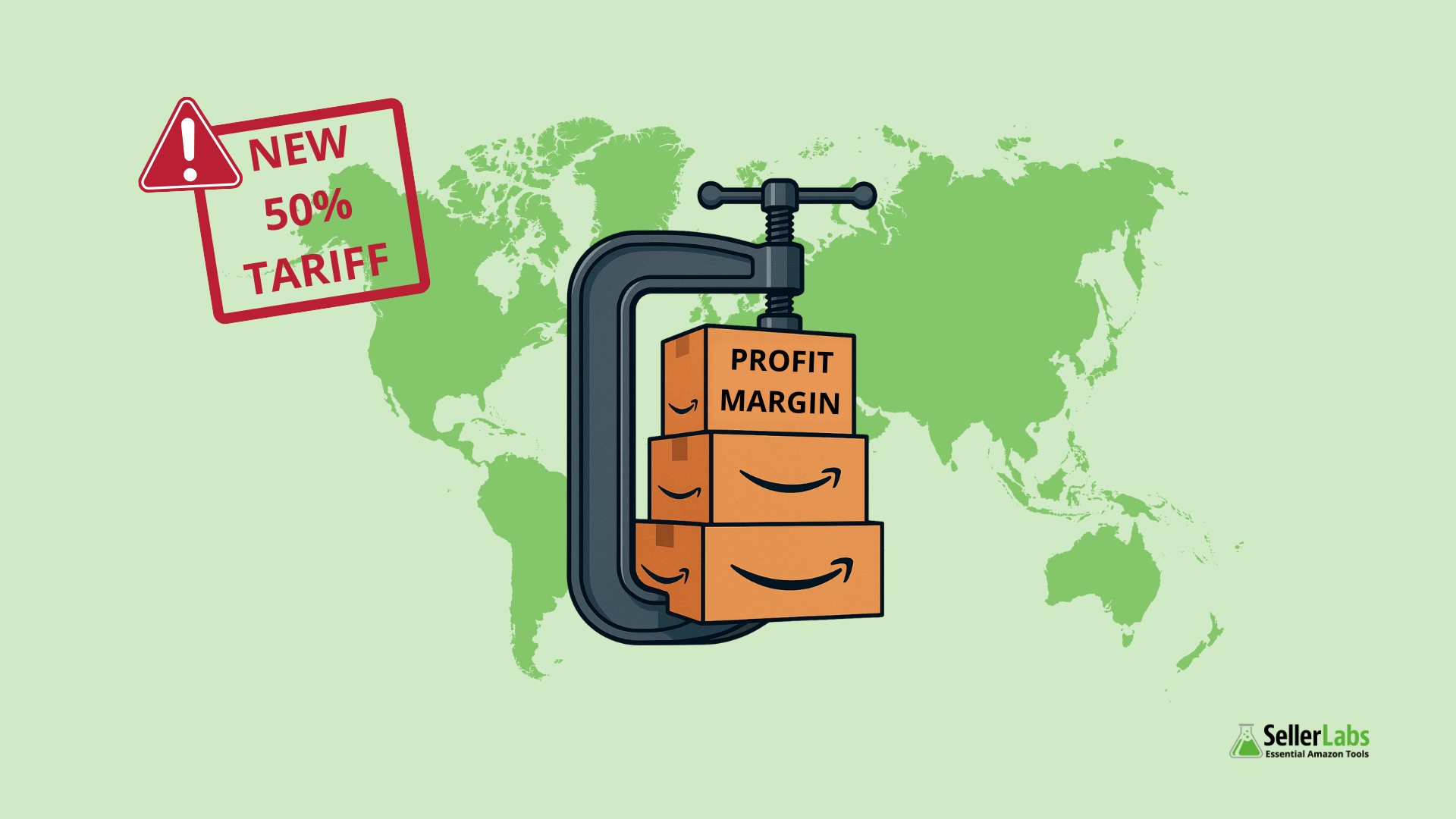

The Trump administration has doubled tariffs on steel and aluminum imports to 50%, effective May 30, 2025. While the policy is framed around national security and revitalizing U.S. manufacturing, it has ripple effects across nearly every industry—especially ecommerce. From canned goods and household tools to sports gear and automotive parts, Amazon sellers will feel the […]

Imagine this: You’re an Amazon seller, and your best-selling product just went out of stock—again. Your PPC costs are rising. You’re buried in support tickets. And you just found out your overseas freight costs jumped 15% overnight. Sound familiar? Here’s the good news: you’re not alone. And better yet—Amazon now offers an entire ecosystem of […]

Why Sustainability Now Matters More Than Ever on Amazon Amazon’s Climate Pledge has gone from an abstract corporate goal to a direct requirement for sellers. As of 2025, Amazon is rolling out stricter guidelines on packaging, carbon emissions reporting, and eligibility for “Climate Pledge Friendly” (CPF) badges. For sellers, this shift is no longer optional. […]

Amazon is overhauling how it reimburses FBA sellers for lost or damaged inventory—and it’s happening right as the marketplace becomes less crowded, but more competitive in different ways. Starting March 10, 2025, reimbursements for inventory lost before a customer order will be based on manufacturing cost, not your retail or sales price. That means if […]

Amazon has changed dramatically over the last few years, but many sellers are still stuck using outdated advice that no longer works. In 2025, clinging to common myths can cost you rankings, profit, and even your account health. Here are 10 Amazon myths that are still floating around and what savvy sellers know to do […]

📉 Noticing fewer impressions, declining sales, or poor ad performance on Amazon? It might not be your price, your product, or even your reviews. It could be Amazon product title suppression—and it’s quietly costing sellers visibility and sales in 2025. The Problem: Amazon Product Title Suppression Is Costing You Sales Amazon has quietly cracked down […]

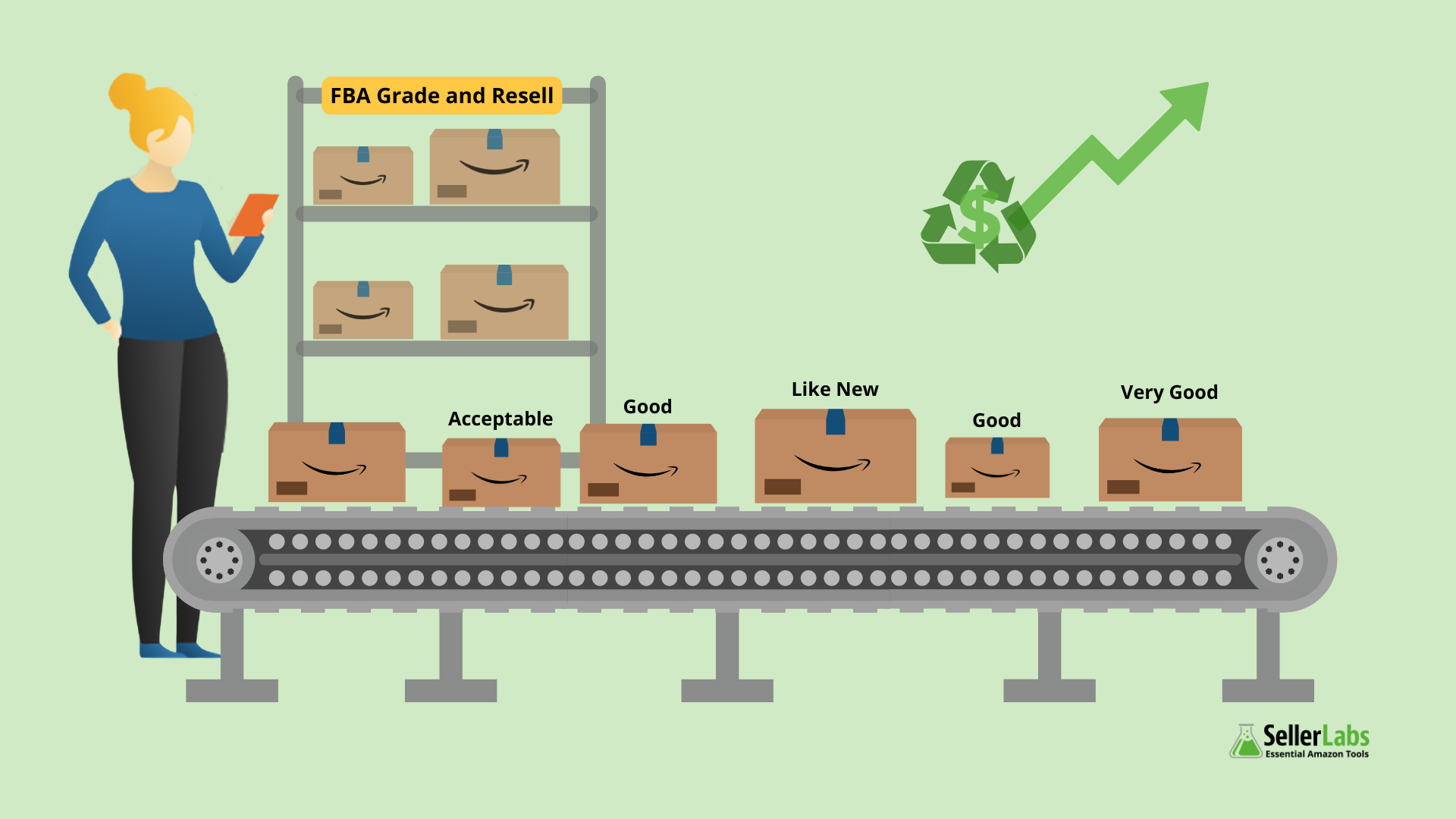

♻️Customer returns don’t have to mean revenue loss. With Amazon’s FBA Grade and Resell program, your returned inventory gets a second chance—and when paired with Seller Labs tools, you can make every relist count. 🎥 Watch Amazon’s official explainer video → What Is FBA Grade and Resell? Amazon’s FBA Grade and Resell program allows sellers […]

Returns are every Amazon seller’s nightmare. In 2025, with stricter policies, rising return rates, and higher fees, sellers are watching profits evaporate. If you feel like you’re losing money on refunds and replacements, you’re not alone. But here’s the good news: there are concrete steps you can take to reduce returns, improve customer satisfaction, and […]

📦 Amazon just reintroduced restock limits—and it’s already disrupting FBA operations for sellers across the board. Here’s what’s changing, how it affects your business, and what you can do to stay in control with Seller Labs. 🚨 What’s Going On? In April 2025, Amazon quietly reactivated restock limits for FBA sellers, capping how much inventory […]

A Temporary Break in the Tariff Storm In a surprise development on May 12, 2025, the United States and China agreed to temporarily slash tariffs by more than 50% for 90 days. While the move is being positioned as a goodwill gesture during ongoing trade negotiations, Amazon sellers importing from China are eyeing this brief […]

If you’re an Amazon seller, you’ve probably felt the pinch of rising FBA fees in 2025. From storage fee increases to new low inventory fees, it’s never been more expensive to use Amazon’s fulfillment services. So the big question is: is Amazon FBA still worth it—or is it time to switch to FBM or a […]

🛑 Still stuck on page two? You’re not alone. In 2025, visibility on Amazon doesn’t come from keywords alone—it comes from what you do outside the marketplace. Let’s break down why external traffic is now critical, how it works, where to drive it from, and how Seller Labs can help you optimize every click. The […]

Amazon has long dominated the e-commerce landscape, but Walmart Marketplace is rising fast. With fewer sellers, lower fees, and Walmart’s massive retail presence, many Amazon sellers are wondering: Is Walmart a better opportunity than Amazon in 2025? Which marketplace offers more profit potential? Let’s break down the key differences to help you decide where your […]

🕓 More days. More buyers. More risk if you’re not ready. 🧠 Prime Day Isn’t Expanding—It’s Evolving In 2025, Amazon isn’t just extending Prime Day from 2 to 4 days—they’re rewriting the seller playbook. This isn’t about a couple of bonus sales days. It’s a complete shift in strategy, buyer behavior, and platform dynamics. For […]

Remember when private label selling on Amazon felt like a digital gold rush? You could slap a logo on a garlic press, run a few giveaways, and suddenly find yourself on Page 1 with profit margins to match. Fast forward to 2025, and the game has changed. Today, with rising Amazon fees, saturated niches, and […]